How does a flood map help canadian home owners?

A flood map shows which areas are prone to flooding in the event of water level rising to a particular elevation. In a nutshell, a flood map provides stakeholders with the necessary data needed to make smart decisions about asset management, urban planning, and flood risk management.

In terms of insurers, up-to-date flood maps enable them to more accurately assess their risks when considering flood insurance options.

Recognizing that on a federal level, Canada lacked effective flood hazard maps, IBC along with other partners, collaborated on a national flood program led by the private sector. And their main focus was the creation of current flood maps.

These maps took into account river gauge and rainfall data to measure flood extent and depth, flood defense information, historical flood records, snowmelt and terrain data. And then incorporated address data, residential replacement costs, and peril information.

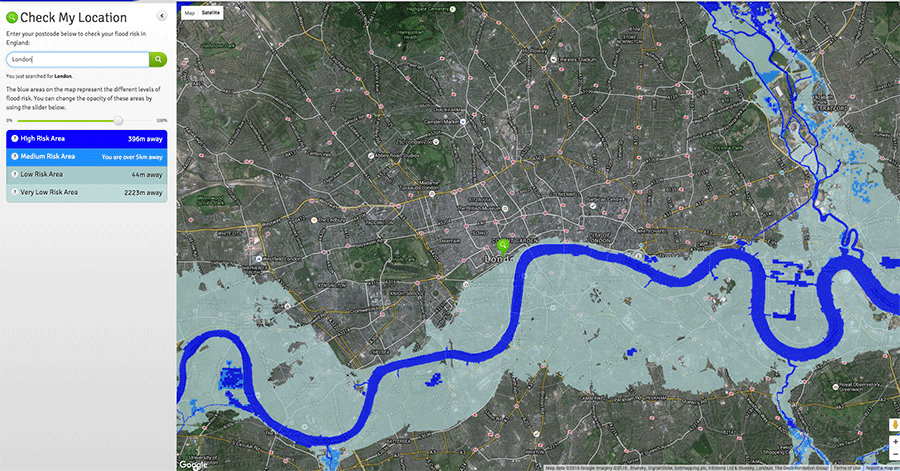

In other countries, like the UK, there are online tools that allow anyone to view the flood risk for their particular region. Simply enter in your location and you can view a very detailed map that highlights likely risk areas. This is certainly a feature any homeowner would review when weighing the pros and cons of relocating to a specific area.

Source

What does this mean for home owners?

As of February 2016, the IBC now has flood maps that let the bureau and insurance companies assess the flood risk right down to the residential level for both fluvial flooding (which occurs when excessive rainfall over an extended period causes a river to exceed its capacity) and pluvial or surface water flooding (caused when heavy rainfall creates a flood event independent of an overflowing water body).

The data revealed that 20% of Canadian households could be qualified as high-risk, and of those, 10% could be considered very high risk. That’s 1.8 million households.

In 2009, the United States Global Research Program determined that the average precipitation in the U.S. has increased approximately five percent the past 50 years, which leads to increased danger of floods.

Changes in land use also contribute to the potential for flooding; as an area becomes built up, there is less permeable land available to absorb water. Both the U.S. and Canada have seen their urban centers become denser with the sprawl reaching further from the downtown cores.

No big deal, you may say. Most people, don’t believe that a flood will ever affect them. It’s an event that they watch on the news.

Flood zone determination

Even if it’s statistically unlikely that you’ll be the victim of a flood, it’s unwise to ignore the possibility, because if it does happen, it can wipe out possessions or investment properties in a matter of minutes.

In fact, even though you may consider your property to be at low risk, flood risk is spread across all types of terrain, across income levels and in both rural and urban locations. Some insurers are finding themselves paying more for sewage backups, given that the infrastructure in many municipalities can be overwhelmed by torrential downpours.

If flood insurance is available to you, you may want to consider it if you are endangered or feel vulnerable. The first step is to determine if you live in a flood zone.

You can also check how likely flooding is in your area using this flood risk finder tool. The Government of Canada is still rolling it out on a province-by-province basis, so it’s worth checking back if your province’s data isn’t available yet.

Flood zone maps – the US model

The United States has flood maps available online for homeowners to review. Flood maps indicate which areas generally flood if water rises to a certain level. They allow both homeowners and policymakers to make informed decisions about asset management, urban planning, and flood risk management.

The Federal Emergency Management Agency (fema.gov) provides flood mapping services and their maps form the basis for flood insurance rates. More than 20,000 U.S. communities have been placed into flood zones, allowing homeowners there to participate in the National Flood Insurance Program. Insurance rates are determined by risk of flooding. In the two most risky flood zones (V and A), homeowners must ensure that:

The lowest floor elevation must be at or above the base flood elevation — the computed elevation to which floodwater is anticipated to rise during the base flood.

Enclosed areas below the lowest floor can’t be use as living space.

Electrical, heating, ventilation, plumbing and air-conditioning facilities must be elevated to or above the base flood elevation.